2.0 BASIC AND FIXED INCOME INVESTMENTS

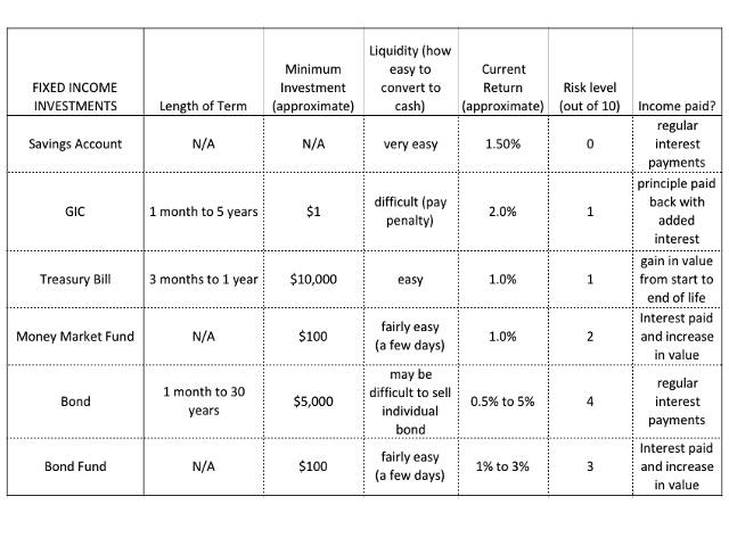

If you’re looking for short term, no-risk investing, fixed-income investments are by far the safest and the simplest of investing tools. They are called "fixed-income" because they provide a steady, known and guaranteed form of income. This chart sums up the different types of fixed-income investments that we'll be talking about:

2.0 Some Basic Terms

Investopedia.com defines inflation: “As inflation rises, every dollar will buy a smaller percentage of a good. For example, if the inflation rate is 2%, then a $1 pack of gum will cost $1.02 in a year.” You may have heard extreme cases of inflation called hyper-inflation where government treasuries print enormous amounts of money in hopes of fixing their hurting economy to the point that a cup of coffee costs a wheelbarrow full of bills! For instance in 1923 the exchange rate in Germany was 4,200,000,000,000 Marks to 1 US dollar. Inflation is a very important phenomenon as it can disguise the real returns of your investments. If your high interest savings account provides a 2% interest rate but the current inflation rate is 2.5%, technically you’re losing 0.5%! So that means you have to beat inflation to get ahead. Given our current economic conditions, this presents an issue with fixed income investments like GIC’s and money market accounts that provide interest rates hovering just above the inflation rate. Note the current inflation rate in Canada is around 1.2%. (September/October 2012) and the historical average from 1915-2012 in Canada is about 3.2%. For interest's sake the highest recorded inflation was 21.6% in 1920 and lowest was -17.8% in 1921... the very next year! So make sure to always keep in mind the effects of inflation when you’re adding up all your assets. You may not be as ahead as you thought. |

These terms are thrown around a lot in the financial world: ASSET – An asset is an object or resource that a person, company or country owns and is used to make profit. Anything from the office building to the office stapler are assets. LIABILITY – A liability is debt or an obligation. An individual would have a debt in form of a mortgage or a bank loan to start a small business; a company would have liability as loans, accounts payable and outstanding money owed to suppliers. Having liabilities are necessary to the growth and operation of a business! SECURITY – A general term for ownership of a financial instrument like stocks, bonds or Treasury Bills. The person or company who sells the stock is called the ‘issuer’ of the security. EQUITY – Equity is a specific type of asset. It represents assets that a person or company owns that have all the associated debts paid off. So a car or house that is completely paid off is equity. Stocks are equity because they are fully paid-for ownership in a company. |

2.1 Your Savings Account

A savings account can be just as important as any other investing tool. For one reason as I mentioned earlier, if you plan on using your savings in the next couple years, your best bet is to keep it safe in a savings account or another low-risk investment.

Second, depending on interest rates, your savings account might be your most valuable money making tool. Currently typical savings accounts pay a rock-bottom 1% interest (pretty much matching inflation), but look at 1981- interest rates peaked at about 21%! (source: Bank of Canada) You’d be lucky to get that kind of return on the stock market. So don’t rule out the trusty old bank account, besides, your money is better off there than tied up on a credit card.

Second, depending on interest rates, your savings account might be your most valuable money making tool. Currently typical savings accounts pay a rock-bottom 1% interest (pretty much matching inflation), but look at 1981- interest rates peaked at about 21%! (source: Bank of Canada) You’d be lucky to get that kind of return on the stock market. So don’t rule out the trusty old bank account, besides, your money is better off there than tied up on a credit card.

2.2 Canadian Money Market

What is the Money Market?

Money Market investments are a generic name for a bunch of different 'debt securities.' And a debt security simply means that somebody, whether it be a person or company or bank, borrows money from you (they're in debt to you) with promises that they'll pay you back with added interest anywhere from 24 hours (short-term) to 5 years (long-term) down the road. They come in many different forms with names like: commercial paper, certificates of deposit (GIC’s), bankers' acceptances, and federal and provincial treasury bills (T-bills).

What are the different types of Money Market investments?

There's a lot of different types of these investments, so I’ll discuss just three of the major ones:

Minimum investment required: $10,000 (ouch)

Cost to buy: none

Current return: ~1.0%

Risk: 0/10

Liquidity (how fast can you convert it to cash): Very liquid, cash the next business day

Length of term: 3 months, 6 months or 1 year

Where to buy: Major banks

Income: The difference between your 'purchase price' and 'par value' is your return (check example below)

T-bills are simply a way for the government to raise money to fund various financial ventures. Since they are through the federal government these are considered the lowest-risk security out there, as both the principal and interest rate are 100% guaranteed. They are issued as three-month, six-month and one-year time frames.

How it works: you purchase a T-bill for a price that’s less than their par (or face) value, then when they reach their maturity date (the date they pay back your money) the government pays the holder the full par value. So for example, if you buy a 3-month T-bill with a face value of $10,000 and you pay only $9,800 at the time of purchase, you will have earned $200 in 3 months.

T-Bills can be converted to cash very quickly, which is why many investors prefer having T-bills instead of cash. But a major con to T-bills is that they can be a little restrictive to those of us just starting out: the minimum investment for a Treasury Bill in Canada is normally $10,000 (according to the Royal Bank of Canada). Yikes!

Also note that since T- Bills are distributed by government agencies, the returns you make are usually only taxed at the federal level; at the provincial and municipal level they are tax-free.

More basics on Treasury Bills:

Watch this great video for a simple explanation of a US Treasury Bill http://www.investopedia.com/video/play/treasury-bill/#axzz2FRPqReJ7

Money Market investments are a generic name for a bunch of different 'debt securities.' And a debt security simply means that somebody, whether it be a person or company or bank, borrows money from you (they're in debt to you) with promises that they'll pay you back with added interest anywhere from 24 hours (short-term) to 5 years (long-term) down the road. They come in many different forms with names like: commercial paper, certificates of deposit (GIC’s), bankers' acceptances, and federal and provincial treasury bills (T-bills).

What are the different types of Money Market investments?

There's a lot of different types of these investments, so I’ll discuss just three of the major ones:

- Canada Treasury Bills (T-Bills)

Minimum investment required: $10,000 (ouch)

Cost to buy: none

Current return: ~1.0%

Risk: 0/10

Liquidity (how fast can you convert it to cash): Very liquid, cash the next business day

Length of term: 3 months, 6 months or 1 year

Where to buy: Major banks

Income: The difference between your 'purchase price' and 'par value' is your return (check example below)

T-bills are simply a way for the government to raise money to fund various financial ventures. Since they are through the federal government these are considered the lowest-risk security out there, as both the principal and interest rate are 100% guaranteed. They are issued as three-month, six-month and one-year time frames.

How it works: you purchase a T-bill for a price that’s less than their par (or face) value, then when they reach their maturity date (the date they pay back your money) the government pays the holder the full par value. So for example, if you buy a 3-month T-bill with a face value of $10,000 and you pay only $9,800 at the time of purchase, you will have earned $200 in 3 months.

T-Bills can be converted to cash very quickly, which is why many investors prefer having T-bills instead of cash. But a major con to T-bills is that they can be a little restrictive to those of us just starting out: the minimum investment for a Treasury Bill in Canada is normally $10,000 (according to the Royal Bank of Canada). Yikes!

Also note that since T- Bills are distributed by government agencies, the returns you make are usually only taxed at the federal level; at the provincial and municipal level they are tax-free.

More basics on Treasury Bills:

Watch this great video for a simple explanation of a US Treasury Bill http://www.investopedia.com/video/play/treasury-bill/#axzz2FRPqReJ7

- GIC’s (Called CD’s in the US)

Stands For: Guaranteed Investment Certificate

Minimum investment required: ~$10

Cost to buy: No cost

Current return: 1.8 to 2.5% (source: Ally Bank of Canada 2012)

Risk (out of 10): 1/10

Liquidity: You have to wait until the maturity date or pay a penalty fee

Length of term: 1 month to 5 years

Where to buy: Most large financial institutions

Income: The principal plus interest is given back at the end of maturity

A G.I.C. (Guaranteed Investment Certificate) is a certificate of deposit issued by a financial institution.

Key points about GIC’s:

- Terms from 1 month to 5 years, where the longer the term, the higher the interest rate

- You can’t withdrawal or deposit into a GIC once it’s opened, the initial amount just sits there until its completion date

- If you need to withdraw the money before the maturity date, you may not receive your interest or you might even pay a penalty

- Essentially a zero-risk investment (insured by banks)

Like most Money Market investments, they currently pay slightly higher than a high-interest savings account. The only advantage to a GIC is if you suspect interest rates to drop, you can lock in the current rate. Maybe if you’re a spontaneous shopper you can use GIC’s to lock away your money so you don’t spend it before an important purchase!

GIC Tip:

Try buying a 5-year GIC once a year, starting now. That way, starting in 5 years you will have a steady flow of income every year at the highest possible interest rate. (Remember 5-year GIC's pay the best interest rates)

|

|

- Money Market Mutual Funds

Cost to buy: 'No-load' funds have no cost to buy, load funds cost $$

Current average return: ~1%

Risk (out of 10): 1/10

Liquidity: A few days to sell mutual funds

Length of term: N/A

Where to buy: Major banks

Income: Interest is accumulated daily and paid to fund-holders monthly, usually automatically in the form of new units in the fund

There aren’t a whole lot of banks, even the big ones, which make it easy to invest in the money market and T-bills. Besides GIC’s, the best way to get into the money market is with money market mutual funds, or sometimes a money market bank account. A money market fund is a mutual fund where a fund manager pools your money along with thousands of other investors and invests in hundreds of different short-term securities, like T-Bills and so on. This helps both to avoid the intimidating $10,000 starting price of T-bills and diversifies your money over many different investments. Talk to a bank investor if this interests you!

Key points about money-market funds:

- Since they are short-term securities, it’s a great place to put your money if you need it in the near future

- Research the management fees before you buy

- T-Bill funds are the safest but are all very low reward

- The shorter the terms, the lower the risk (as well as reward)

- Buy a no-load fund (no cost to buy the fund) Historically load funds do not outperform no-load funds anyway!

The main disadvantage of a money-market fund, especially in today’s conditions, is since it is such a low-risk fund the payout will be low. So you might want to explore other options if you can stomach a bit more risk.

More basics on Money Market:

Investopedia Money Market explained: http://www.investopedia.com/university/moneymarket/default.asp

2.3 Bonds and Bond Funds

Minimum investment required: individual bonds- ~$5000, bond funds- ~$250

Cost to buy: individual funds: no cost, bond funds: cost of fund purchase

Current return: ~0.5% to 6% (wide range)

Risk (out of 10): 3/10

Liquidity: not great, can be tricky to sell individual bonds

Length of term: 1 month to over 30 years

Income: regular interval interest payments (ex. semi-annually)

Cost to buy: individual funds: no cost, bond funds: cost of fund purchase

Current return: ~0.5% to 6% (wide range)

Risk (out of 10): 3/10

Liquidity: not great, can be tricky to sell individual bonds

Length of term: 1 month to over 30 years

Income: regular interval interest payments (ex. semi-annually)

What is a bond?

Compared with the exciting and ever-changing world of the stock market, bonds are sort of the boring cousin, which in some cases can be a good thing for your portfolio. A bond is essentially a fancy IOU. Businesses and banks borrow your money to either fund their business operations or invest in other assets and in return for the nice favor they’ll pay you interest every so often. In the world of bonds this interest is called the coupon. The date a bond expires, usually called the maturity date, can vary from one month (short-term bond) to more than 30 years (long-term bond). At the maturity date you’ll receive

your initial principle back in full plus your interest, like if you buy a 10-year bond for $1000

you’ll get exactly $1000 back in 10 years plus interest. Simple as that.

Compared with the exciting and ever-changing world of the stock market, bonds are sort of the boring cousin, which in some cases can be a good thing for your portfolio. A bond is essentially a fancy IOU. Businesses and banks borrow your money to either fund their business operations or invest in other assets and in return for the nice favor they’ll pay you interest every so often. In the world of bonds this interest is called the coupon. The date a bond expires, usually called the maturity date, can vary from one month (short-term bond) to more than 30 years (long-term bond). At the maturity date you’ll receive

your initial principle back in full plus your interest, like if you buy a 10-year bond for $1000

you’ll get exactly $1000 back in 10 years plus interest. Simple as that.

So, what types of bonds are there?

Bonds come in two main types:

When you loan money to a government agency like the Treasury Department (the guys who print the money), the risk is significantly lower than if you buy a bond through a small company because, well, the Treasury can just print more money! So Treasury bonds are pretty close to guaranteed.

Let’s compare those government bonds with the riskiest form of bonds: low-grade corporate bonds, also known as high-yield or junk bonds. Here you loan your money to smaller, riskier corporations that could possibly experience some financial turmoil. But for your increased risk the reward is normally several percentage points higher. The third bond type that sits right in the middle of the risk spectrum are high-grade corporate bonds that deal with large blue chip companies (blue chip company: nationally recognized, well-established and financially sound companies like Wal-Mart and Coca-Cola).

What’s the risk of bonds?

1. Interest Rates

Another feature of bonds is that you can buy or sell them just like stocks before they hit their maturity date. Keep in mind though that bond prices can fluctuate just like a stock- but instead of fluctuating due to a company’s earnings, bond prices change because of rises and falls in interest rates. Bonds share an inverse relationship with interest rates: when interest rates rise, bond value falls and vice versa. It’s a confusing concept so I’ll explain with an example. Suppose you buy a 10-year bond that yields 8% interest. Then in one year the rate on a similar new bond is 4%. Well your bond looks pretty great to other people now, right? You have a fine-looking 8% yield while everyone else is buying 4% yield bonds. Therefore investors are willing to pay more for your valuable bond and so it is worth more if you were to sell it. So as I said: interest rates fall, bonds value goes up.

Speculators try and predict the future: they scoop up bonds just before they believe interest rates will fall, resulting in their bonds value going up. In my opinion, no one can predict the future and this strategy is not that much different from the roulette table, but each to their own.

2. Inflation

So then what’s the risk if I decide to just hold on to my bond for its entire term? The risk is inflation. Let’s look at another example: assume your $1000, 10-year bond pays 3% interest but inflation rates shoot up to 4%, then for the next 10 years you would be stuck earning -1%! Plus your $1000 you get back at the end will have a lot less value or ‘purchase power’ due to the inflation.

Check out Six Bond risks from Investopedia: http://www.investopedia.com/articles/bonds/08/bond-risks.asp#axzz2FRPqReJ7

Other stuff about bonds:

Final Words:

As far as overall risk is concerned, bonds fall somewhere between high-risk stocks and no-risk investments like GIC’s and your savings account. They fluctuate less than stock prices but aren’t entirely risk free; your success in bonds will be influenced by rising and falling national interest rates, as well as inflation.

Many investing guides will tell you that you should have part of your portfolio in some form of bond for diversification. One rule of thumb is to use your age as percentage, so at 40 years old have 40% in bonds. Keeping in mind that buying an individual bond can cost you over $5000 you might want to think about a low-cost Mutual Fund in bonds or a Bond ETF like iShares Universal Bond Index (XBB) which invests in hundreds of different bonds and only costs maybe $100 to get started.

More on the basics of Bonds:

CNN Money 101: http://money.cnn.com/magazines/moneymag/money101/lesson7/index4.htm

Investopedia: http://www.investopedia.com/university/bonds/#axzz2FRPqReJ7)

Head over to the Mutual Funds and ETF's tab to keep going! ----->

Bonds come in two main types:

- Treasury and government bonds

When you loan money to a government agency like the Treasury Department (the guys who print the money), the risk is significantly lower than if you buy a bond through a small company because, well, the Treasury can just print more money! So Treasury bonds are pretty close to guaranteed.

- Corporate Bonds

Let’s compare those government bonds with the riskiest form of bonds: low-grade corporate bonds, also known as high-yield or junk bonds. Here you loan your money to smaller, riskier corporations that could possibly experience some financial turmoil. But for your increased risk the reward is normally several percentage points higher. The third bond type that sits right in the middle of the risk spectrum are high-grade corporate bonds that deal with large blue chip companies (blue chip company: nationally recognized, well-established and financially sound companies like Wal-Mart and Coca-Cola).

What’s the risk of bonds?

1. Interest Rates

Another feature of bonds is that you can buy or sell them just like stocks before they hit their maturity date. Keep in mind though that bond prices can fluctuate just like a stock- but instead of fluctuating due to a company’s earnings, bond prices change because of rises and falls in interest rates. Bonds share an inverse relationship with interest rates: when interest rates rise, bond value falls and vice versa. It’s a confusing concept so I’ll explain with an example. Suppose you buy a 10-year bond that yields 8% interest. Then in one year the rate on a similar new bond is 4%. Well your bond looks pretty great to other people now, right? You have a fine-looking 8% yield while everyone else is buying 4% yield bonds. Therefore investors are willing to pay more for your valuable bond and so it is worth more if you were to sell it. So as I said: interest rates fall, bonds value goes up.

Speculators try and predict the future: they scoop up bonds just before they believe interest rates will fall, resulting in their bonds value going up. In my opinion, no one can predict the future and this strategy is not that much different from the roulette table, but each to their own.

2. Inflation

So then what’s the risk if I decide to just hold on to my bond for its entire term? The risk is inflation. Let’s look at another example: assume your $1000, 10-year bond pays 3% interest but inflation rates shoot up to 4%, then for the next 10 years you would be stuck earning -1%! Plus your $1000 you get back at the end will have a lot less value or ‘purchase power’ due to the inflation.

Check out Six Bond risks from Investopedia: http://www.investopedia.com/articles/bonds/08/bond-risks.asp#axzz2FRPqReJ7

Other stuff about bonds:

- Most non-treasury bonds will have a rating that rates the riskiness of the bond. This is done by large rating firms like Standard & Poor’s and Moody’s. ‘AAA’ for high quality and ‘D’ for default.

- There are both fixed and variable rate bonds. Fixed rate bonds are essentially GIC’s as they are guaranteed interest rates, but with less risk the payout is of course lower than variable rate bonds

- Typically the interest rates on long-term bonds are higher than short-term because the longer you have a bond, the longer you would be stuck with it if interest rates go up. For instance, if you own a 10-year bond at 3%, and over the next 10 years interest rates shoot up to 8%, you’re stuck with your measly 3% for a lot longer than if you just had just a 5-year bond. More risk, more reward.

- Some bonds issued by a provincial or city agency are tax free. These pay less than taxable bonds but for people in high tax brackets it can be quite appealing

Final Words:

As far as overall risk is concerned, bonds fall somewhere between high-risk stocks and no-risk investments like GIC’s and your savings account. They fluctuate less than stock prices but aren’t entirely risk free; your success in bonds will be influenced by rising and falling national interest rates, as well as inflation.

Many investing guides will tell you that you should have part of your portfolio in some form of bond for diversification. One rule of thumb is to use your age as percentage, so at 40 years old have 40% in bonds. Keeping in mind that buying an individual bond can cost you over $5000 you might want to think about a low-cost Mutual Fund in bonds or a Bond ETF like iShares Universal Bond Index (XBB) which invests in hundreds of different bonds and only costs maybe $100 to get started.

More on the basics of Bonds:

CNN Money 101: http://money.cnn.com/magazines/moneymag/money101/lesson7/index4.htm

Investopedia: http://www.investopedia.com/university/bonds/#axzz2FRPqReJ7)

Head over to the Mutual Funds and ETF's tab to keep going! ----->

Pic from here